IRS Notice CP53E: Why you received a refund for your underpayment penalty

If you recently paid your tax bill early but received a letter from the IRS titled Notice CP53E, you might be understandably confused. The notice states: “We couldn’t direct deposit your 2025 Form 1040 refund.” “Wait – if I owed money and paid it, why is the IRS trying to send me a refund, and why couldn’t they deposit it?” you may ask. Here is exactly what is happening behind the scenes, and why this is actually a “good” notice.

Why do I have a refund if I owed taxes?

When you owe taxes at the end of the year, you are often subject to an “estimated tax underpayment penalty,” whic is interest charge accruing on a daily basis. Calculating this penalty is where things get tricky.

The IRS allows tax preparers to leave the penalty calculation blank and let the IRS send the taxpayer a bill later. While this is a common industry practice, our client surveys show that people absolutely hate receiving surprise bills from the IRS. Furthermore, if an IRS bill is not addressed promptly, additional penalties are added on top of the original penalty, and the IRS can eventually freeze your bank accounts or garnish your paycheck.

To protect you from escalating penalties and surprise bills, our practice is to have you pay the penalty together with the tax owed when you file. However, unlike a fixed tax amount, we cannot calculate the penalty exactly to the penny because we do not know the exact date the IRS will clear your payment and stop charging interest.

To ensure you never receive a balance-due notice, we overestimate the penalty by calculating it all the way to the April 15th deadline. When you pay early and the IRS clears your payment before April 15th, they recalculate the penalty based on the exact date they received your funds. Because of our built-in buffer, the IRS realizes you overpaid the penalty and sends you a refund! For example, on a $17,000 underpayment paid two weeks early, the refunded interest is about $50.

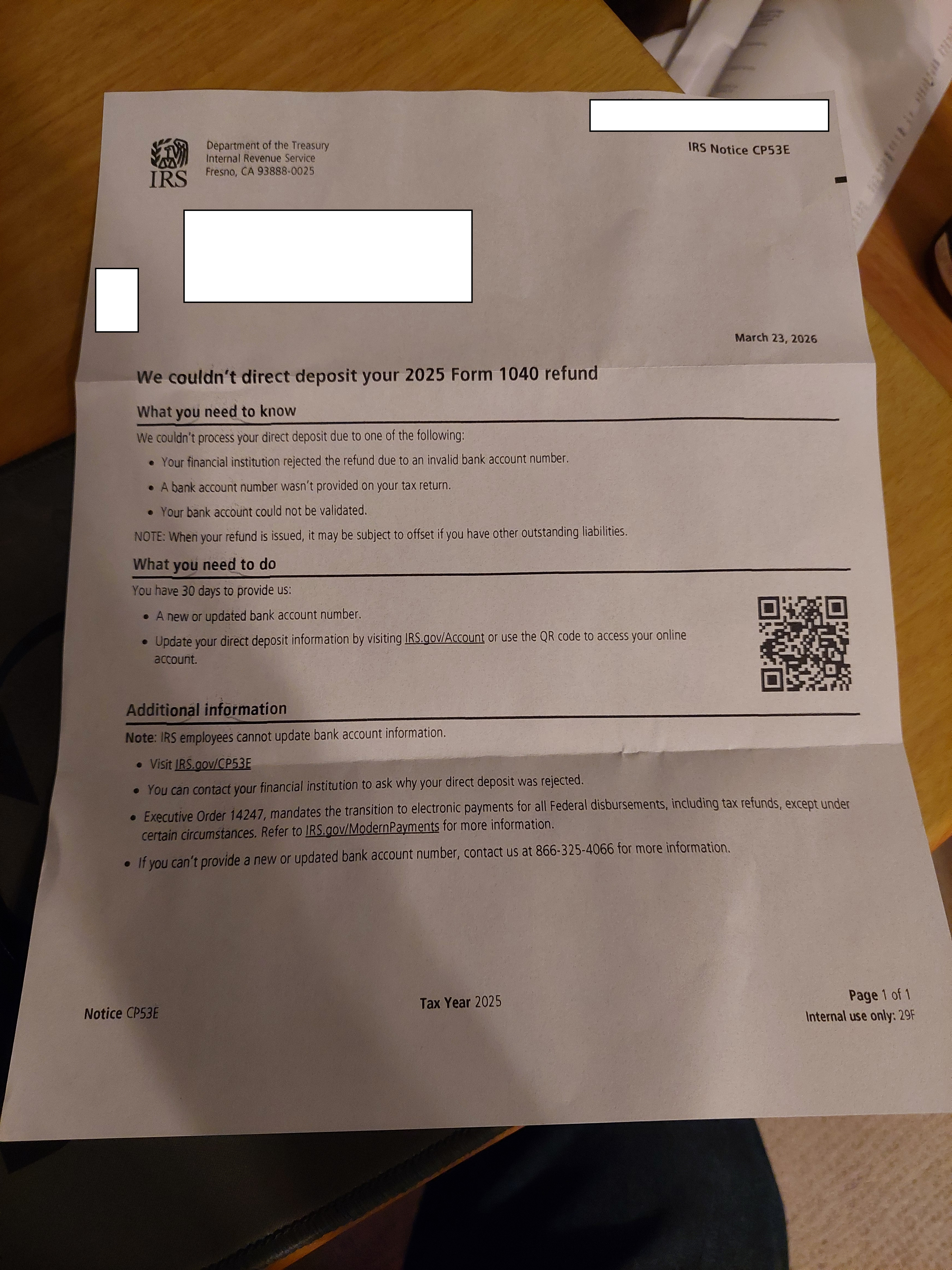

What is Notice CP53E?

Notice CP53E is generated when the IRS owes you a refund but does not have valid banking information on file to direct deposit the money.

Because your tax return originally showed a balance due, IRS e-file rules dictate that we cannot include direct deposit information for a refund on your return. The bank information you provided to pay your tax bill acts as a one-time authorization for the IRS to withdraw funds; the IRS system does not automatically use that same account to deposit funds back to you.

The CP53E letter simply gives you 30 days to log into your secure IRS.gov account and provide a bank account number so they can send you your money. If you do not respond, the IRS will eventually issue a paper check, though this process is significantly delayed due to recent federal mandates prioritizing electronic payments.

Why this is the safest approach

Our “safe buffer” strategy is the best option to protect your financial health. Even if you take no action and ignore the Notice CP53E, it does not impact you negatively: you will not be charged further penalties, and your payroll and bank accounts remain completely safe from IRS levies. You simply get your small refund slightly later.

However, the absolute best option is to not owe an underpayment penalty in the first place! Please refer to this post to find out how to adjust your withholdings so you never have to deal with tax penalties again.